As your real estate appreciates, you may be thinking about how to manage your assets...

Read MoreSo, you are looking to sell your investment property and do a 1031 exchange. You might be just starting to explore the idea, or already have listed your property on the market. What you want to do now is find out which replacement rule is right for you.

In a 1031 exchange, there are three rules that govern the identification of replacement properties, but you only have to follow one of these rules. There are different identification methods for different situations, and this article will explore them to see what is best for you.

Most investors, depending on their situation, will follow the three property rule or the 200% rule. If you want a recap of what a 1031 exchange is, you can click here.

Note: Remember you have 45 days to identify your potential replacement property and 135 additional days to close on that property. A total of 180 days to do your 1031 exchange from the date of your relinquished property. You will want to send your property identification to your qualified intermediary (QI). QI’s can have different ways of having you provide your identification information. Some will have you fill out a form. Talk to your QI about their process and seek professional help if you have any questions.

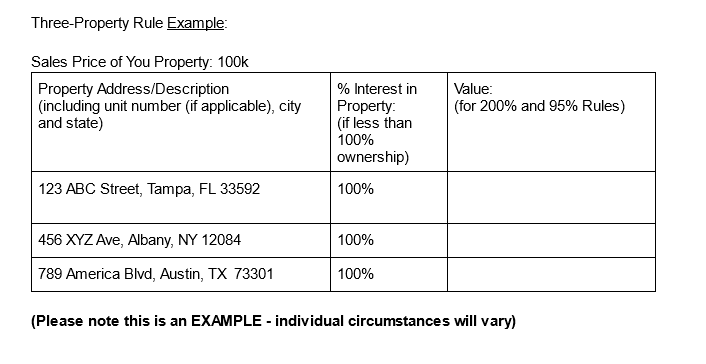

Three property rule:

Under this rule, the investor can identify up to three potential replacement properties, regardless of their value. The investor must purchase one or more of the identified properties in order to complete the exchange. In other words you can identify three properties without regard to the fair market values of the properties. You can acquire one, two, or even all three of the properties. This is one of the more used identification rules.

In the example above you can see three properties identified. It is important to note that in order to do a complete and successful exchange you must purchase replacement property of equal or greater value of the property you sold. In this example above assume all properties met that condition. Therefore, closing on any one of these would complete your exchange.

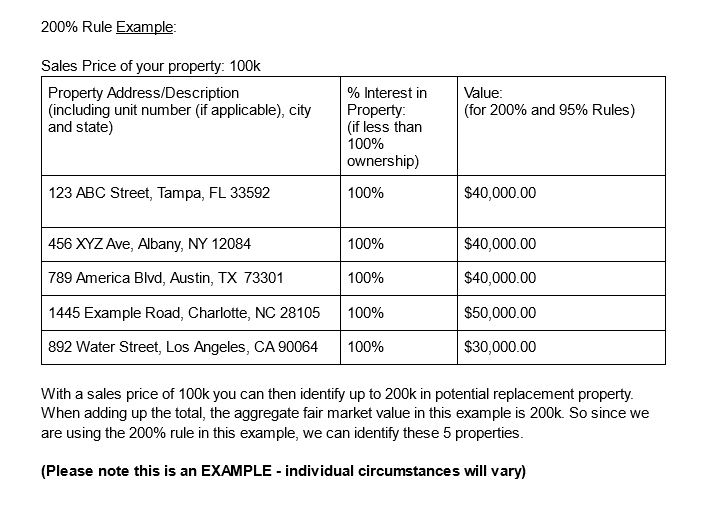

200% rule:

Under this rule, the investor can identify any number of potential replacement properties, as long as the total fair market value of all identified properties does not exceed 200% of the value of the relinquished property. This rule allows investors to identify more properties if the value of the identified properties is lower than the value of the relinquished property. This rule is used when looking at exchanging into multiple smaller properties or fractional interest’s.

95% rule:

Under this rule, the investor must acquire at least 95% of the value of the identified replacement properties by the end of the exchange period. This rule is designed to ensure that the investor has a high degree of certainty that the exchange will be completed. This rule is primarily used by institutions and large scale investors.

If an investor fails to follow the rules and requirements for a 1031 exchange, the exchange may not qualify for tax-deferred treatment, and the investor may be subject to capital gains tax and other taxes on the sale of the original property. Specifically, the investor may have to pay taxes on any capital gains realized from the sale of the relinquished property, as well as depreciation recapture taxes.

In addition, if the investor fails to follow the identification rules, they may be limited in their ability to identify and purchase replacement properties, which could result in the exchange not being completed.

It’s important to work with qualified professionals and follow the rules and requirements carefully in order to ensure that the exchange qualifies for tax-deferred treatment. Investors should consult with a tax advisor, attorney, and qualified intermediary to determine the best strategy for their specific situation and to ensure that they are in compliance with the IRS regulations.